Prescription drug costs are the fastest-growing line item in most employer health plans today. If you're a self-funded employer, that growth hits differently because, unlike fully insured businesses, you are not handing a premium check to a carrier and walking away. Every dollar spent on medications comes directly from your plan reserves. For a troubling number of organizations, a significant portion of that spend is entirely preventable.

The numbers are stark. Prescription drugs account for 18% of total healthcare spending. Because those costs increased by 10.2% in 2024, and projection estimates call for another 9% to 11% increase in 2025, a 300-person company spending $3 million a year on health benefits could face $270,000 in new pharmacy costs next year alone. This is largely driven not by sicker employees, but by a system that has very little incentive to find cheaper alternatives.

Understanding why that happens and knowing where to look is the first step to reclaiming control.

The Hidden Economics of Your Drug Plan

Most self-funded employers contract with a Pharmacy Benefit Manager (PBM) to handle their prescription drug benefit. On the surface, this seems like a straightforward arrangement: the PBM negotiates prices with drug manufacturers and pharmacies, and passes savings along to you.

The reality is considerably more complicated.

PBMs negotiate with pharmaceutical manufacturers for price discounts, which are typically paid as rebates based on sales volumes driven by formulary placement. In exchange for low administration fees, plan sponsors allow PBMs to keep a portion of the negotiated rebates and other fees. Contracts between PBMs and plan sponsors contain rebate guarantees, which perpetuate the demand for high-rebate drugs by encouraging PBMs to maximize rebate revenue. This dynamic gives preference to some drugs over others on formularies based on rebate revenue rather than their value or final cost to the patient or plan sponsor.

In plain English: your PBM may be steering employees toward more expensive drugs because doing so is more profitable for the PBM, not because those drugs are better or necessary.

Additionally, PBMs earn revenue from "spread pricing," the difference between what PBMs pay pharmacies on behalf of plan sponsors and what PBMs are reimbursed by the plan sponsor. This also encourages PBMs to prioritize higher-cost drugs to allow for a larger spread.

This creates a system where the intermediary managing your drug benefit has financial incentives that run directly counter to your interests as the plan sponsor. And because these arrangements are shielded by confidentiality agreements, most employers never see clearly how their money is moving.

The Brand vs. Generic Gap: Bigger Than You Think

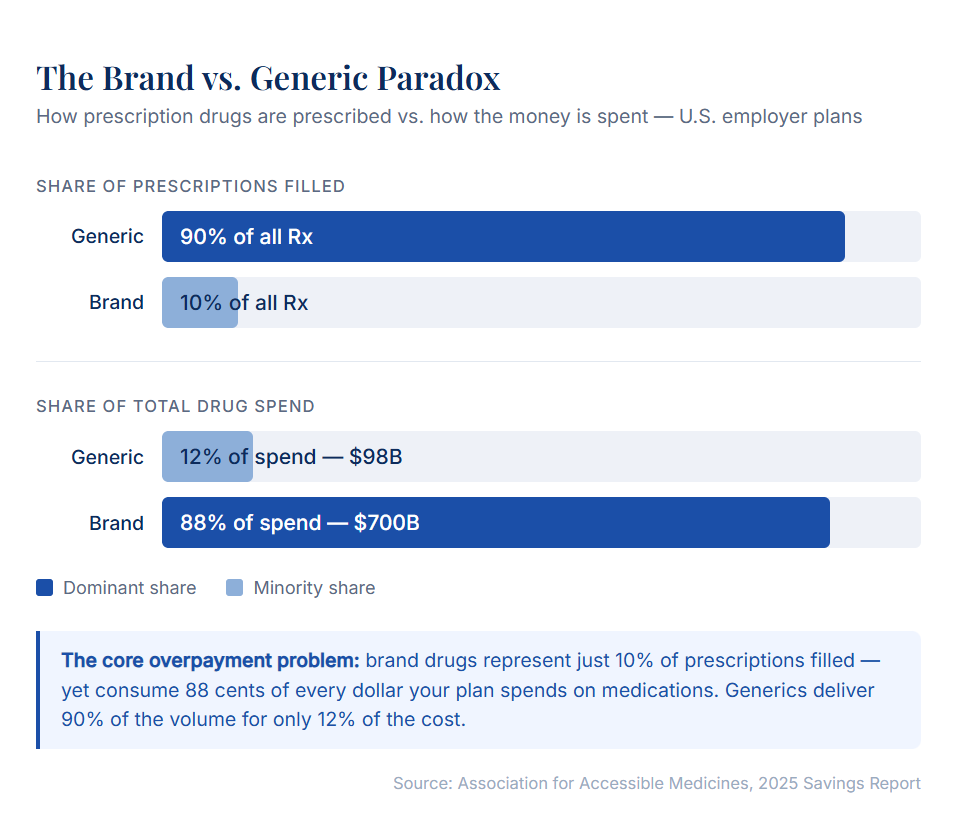

The clearest and most correctable overspend in most employer formularies is brand-name drug usage when generics exist.

The data here should make any CFO sit up straight. In 2024, generics comprised 90% of all prescriptions filled in the U.S., but only 12% of total prescription drug spending. Conversely, brand-name drugs made up only 10% of prescriptions filled, while accounting for a staggering 88% of total spending. Americans spent only $98 billion on generic medicines, but $700 billion on brand-name drug prescriptions.

That ratio of 10% of volume driving 88% of cost is the core of the overpayment problem. In addition, generic drug utilization saves 80% to 85% over brand-name medications.

Let's look at some of the most commonly overpaid drug categories in employer plans:

Statins (cholesterol medications): Atorvastatin, the generic equivalent of Lipitor, is one of the most prescribed drugs in the United States. Even after generics have been widely available, price shopping reveals dramatic variation. Some pharmacy chains priced atorvastatin at $146 for a 30-day supply, while competitors offered the same medication for $18. If employees on your plan are filling brand Crestor or brand Lipitor, or even generics at inflated pharmacy prices, you may be paying 5 to 8 times more than necessary for a cholesterol medication that has been off-patent for years.

Proton pump inhibitors (acid reflux / GERD medications): Brand-name Nexium (esomeprazole) carried a list price well above $200 per month for years after its generic became available for under $20. Plans that fail to enforce generic substitution or tier brand drugs appropriately continue to pay multiples of the true market cost for medications in this class.

Biologics and biosimilars: This is where the largest dollars are often hiding. Consider Humira (adalimumab), one of the world's best-selling drugs, used to treat rheumatoid arthritis, Crohn's disease, psoriasis, and other autoimmune conditions. A one-month supply of brand-name Humira can cost around $7,000 to $13,000 without insurance, and employer plans often bear the bulk of that cost.

Until 2023, Humira had no direct competition in the U.S. AbbVie filed over 130 patents related to Humira, covering not just the drug itself but its manufacturing process, dosing schedules, and even the injector device, successfully delaying competition for nearly 20 years. But that era is over. Multiple biosimilars have now entered the market at dramatically lower prices.

Blue Shield of California struck a deal to purchase an FDA-approved Humira biosimilar for $525 per monthly dose, compared to the market reported net price of Humira at $2,100, which is a 75% reduction for a clinically equivalent product. Yet the state of Tennessee spent $48 million on Humira alone last year, about $62,000 for each of the 775 patients covered by its employee health insurance program, even as biosimilar alternatives were available for as little as $995 a month.

That is not a small oversight. That is the kind of formulary misalignment that costs self-funded plans hundreds of thousands, or even millions, of dollars annually.

The Rebate Trap: When "Savings" Aren't Really Savings

One of the most counterintuitive dynamics in employer pharmacy spending is the rebate check. Many employers receive year-end rebate payments from their PBM and view them as evidence that their plan is being well-managed. The reality is more complicated.

As one benefits executive put it: "The happiest day of a benefit executive's year is walking into the CFO's office with a several-million-dollar check and saying, 'Look what I got you!'" But if the state of Tennessee received a check for, say, $20 million, it was merely getting back some of the $48 million it already spent. Michael Thompson, president and CEO of the National Alliance of Healthcare Purchaser Coalitions, described this arrangement as a "devil's bargain."

Rebates sound like savings, but they are actually a partial refund on a purchase that was overpriced to begin with. A plan that pays $48 million for a drug and receives $20 million back is in a very different position than a plan that simply pays $15 million for a biosimilar equivalent, even though the rebate check feels like a win.

Formularies can contain drugs that have little or no additional clinical value, precisely because those drugs generate larger rebates for the PBM. Unless your plan has full transparency into the net cost of every drug on your formulary, accounting for rebates, spread pricing, and administrative fees, you do not actually know what you are paying.

How Much Is Really at Stake?

The research on employer savings from formulary optimization is compelling.

A study published in JAMA Network Open examined two large, self-insured employers with a combined 360,000 beneficiaries that updated their prescription drug formularies by swapping out costlier drugs with lower-priced but clinically equivalent options. The two employers saved between 9% and 15% on annual prescription drug spending. Among the therapeutic classes targeted, 30-day prescription spending declined by 53% for the first employer and 67% for the second.

Of the 279 drugs replaced with lower-cost options: 26% were brand-name drugs with cheaper generics; 40% were branded or generic drugs with minor chemical differences and a higher cost than their alternatives but no added clinical value; and 29% were same-class products with less expensive alternatives of equivalent therapeutic value.

That last category is critical: nearly 70% of the savings opportunities came not from simple brand-to-generic swaps, but from more sophisticated analysis of therapeutic equivalence across drug classes. This is not something a plan sponsor can easily spot on their own; instead, it requires a systematic review of claims data against a current clinical evidence base.

A separate analysis of 15 self-insured plan sponsors found that reducing the use of high-cost, low-value drugs could lead to $63 million in annual savings across those employers, representing 3% to 24% of overall pharmacy spending, depending on a number of factors.

A 3% to 24% reduction in pharmacy spend. For a mid-sized company, that range starts in the tens of thousands and climbs quickly into the hundreds of thousands.

Five Warning Signs Your Drug Plan May Be Overpaying

Not every employer has the bandwidth to audit their own claims data. But there are practical signals worth paying attention to:

- 1. Your formulary hasn't been reviewed recently. Drug markets move fast. Biosimilars enter. New generics launch. A formulary designed two or three years ago may not reflect today's lowest-cost clinically equivalent options. Generic Crestor, for example, has been available since 2016, but some plans still pay brand-tier rates.

- 2. You don't know your net drug costs. If your PBM reports gross spend and a rebate check, but you can't see the net cost at the drug level, you are managing blind. Transparent, pass-through PBM contracts show you exactly what you paid for each claim, which is the only way to identify overpayment.

- 3. You have employees on biologics without biosimilar review. If anyone on your plan takes Humira, Enbrel, Stelara, or other high-cost biologics, and your plan has not actively reviewed the availability of FDA-approved biosimilars, you are almost certainly overpaying. The savings available here are often the largest single opportunity in a plan.

- 4. Your specialty drug spend is growing faster than your overall claims. Specialty drugs, including biologics, oncology agents, and other high-cost therapies, represent a growing share of total drug spend for most plans. Without specific management strategies for this category, growth tends to outpace even well-managed formularies.

- 5. You rely on a single PBM without benchmarking. The pharmacy benefit management market is competitive, and pricing varies substantially. Plans that haven't benchmarked their PBM contract terms against the market in the past few years are frequently overpaying on dispensing fees, administrative costs, and guaranteed discount rates.

What Effective Drug Plan Management Actually Looks Like

The levers for reducing pharmacy spend are real, measurable, and available to any self-funded employer willing to look at their data honestly.

Effective management starts with claims data analysis, which is a detailed review of what your plan is actually spending, drug by drug, compared to what the lowest-cost clinically equivalent alternative would cost. This is not about cutting benefits or restricting access. It is about ensuring that when your employees pick up a prescription, your plan pays a fair and appropriate price for it.

From there, it typically involves formulary optimization, updating which drugs are preferred on your plan, how cost-sharing tiers are structured, and whether substitution requirements align with current clinical evidence. The Johns Hopkins research cited earlier found that 95% of drugs identified as having lower-cost alternatives were successfully replaced with clinically equivalent options, with no meaningful difference in clinical outcomes.

For plans with employees on specialty medications, biosimilar transition programs are now one of the highest-return interventions available. The Humira example alone, with 22 biosimilar versions now on the U.S. market at prices ranging from 14% to 85% below the brand, illustrates just how dramatic the savings opportunity can be when plans actively manage this category rather than defaulting to brand coverage.

Finally, PBM contract transparency is foundational to all of this. Transparent PBM partnerships reduce costs by 20% to 30% compared to traditional opaque arrangements. Without visibility into what your intermediaries are earning, it is impossible to know whether the incentives in your system align with your plan's interests.

The Bottom Line for Self-Funded Employers

The self-funded model gives employers a powerful advantage: the ability to see their own data and make decisions accordingly. But that advantage is only realized when someone is actually looking at the data, and comparing it against what better options exist.

Pharmacy is the one area of health benefits where the gap between what plans pay and what they should pay is most consistently large, most consistently hidden, and most consistently correctable. The research is clear that the average employer has meaningful savings available, not through benefit cuts, but through smarter purchasing decisions that are already available in the market.

Every time an employee fills a brand-name drug when a therapeutic equivalent costs 80% less, your plan absorbs a cost it didn't have to. Multiply that across your workforce, across a full year, and the numbers add up fast.

The question isn't whether the savings are there. The question is whether your current plan has the visibility to find them.

Analyze your pharmacy claims

Ready to see how much self-funded plans can save on prescription drugs? StreamRX helps you secure the best pass-through rates and terms.

Explore Self-Funded Plans